GUEST SUBMISSION: On Monday June 1, CMHC announced that operating expense benchmarks were increasing for five-plus-unit multifamily insured mortgages with the changes taking effect for applications received on June 8 or later.

These higher expense benchmarks may result in lower loan amounts. CMHC last updated these benchmarks three years ago in 2023.

For context, when underwriting expenses on multifamily properties, CMHC generally takes actuals or appraiser-projected expenses for property tax, utilities and insurance.

However, for maintenance & repair, property management, salaries, replacement reserves and miscellaneous costs, CMHC generally uses the higher of actuals or benchmark expenses.

Expenses can vary by owner

This is due to the fact that these expenses can vary based on each owner.

For example, some owners may self manage a building or defer maintenance whereas another owner may hire a third party manager and

have regular maintenance. Different owners may also have different accounting treatment or allocations for repairs and maintenance. In the event of default, third party property management would likely be required.

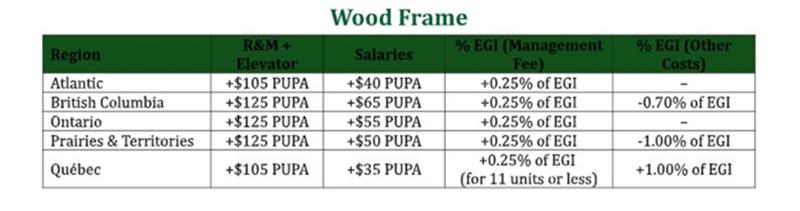

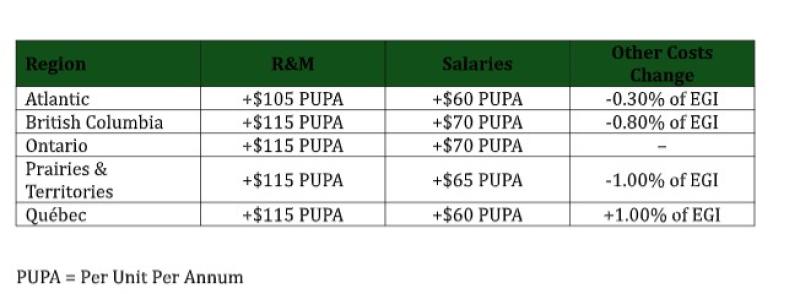

These benchmark expenses vary by building type (wood frame vs concrete) and by region. The changes which came into effect on June 8 are outlined below.

Wood Frame

Concrete

These adjustments to CMHC operating expense benchmarks across Canadian markets are starting to influence loan sizing outcomes across asset classes and regions. By holding all other variables constant — including taxes, insurance, utilities, interest rates and capitalization assumptions — this analysis isolates the direct impact of benchmark-driven changes in operating expenses on achievable loan proceeds across varying average rent per unit levels in comparison to previous benchmarks.

The summary below highlights these effects.

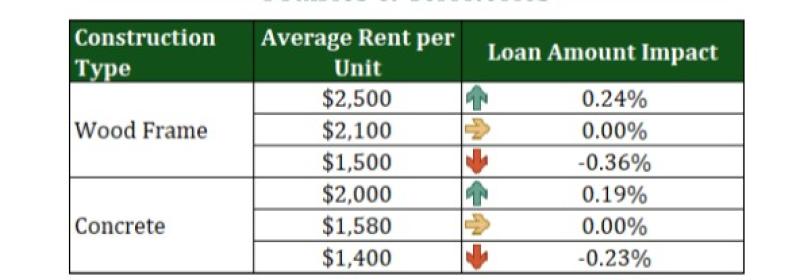

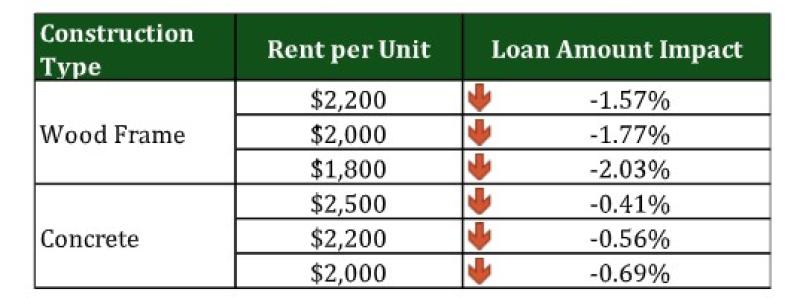

Prairies and Territories

Insight: Prairies remain the most stable region with minimal loan sensitivity across both construction types.

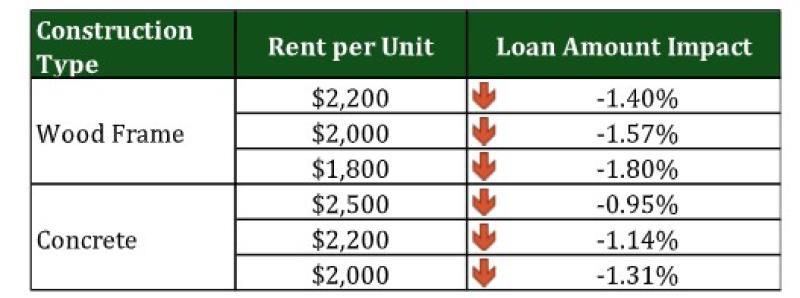

British Columbia

Insight: For wood frame, overall loan amounts trend downward as other benchmark increases outweigh operating cost decrease. For concrete buildings, there is minimal loan sensitivity.

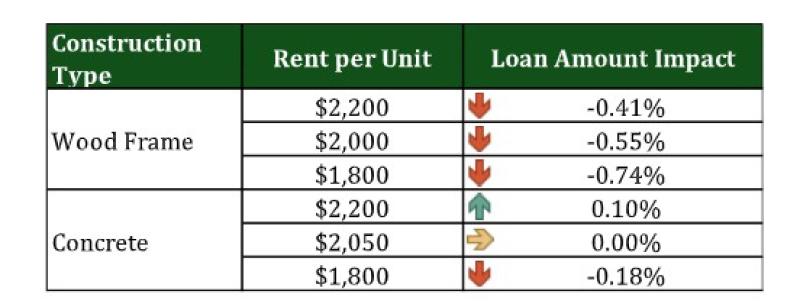

Atlantic

Insight: Benchmark increase is reducing loan proceeds for both construction types.

Ontario

Insight: Benchmark increase is reducing loan proceeds for both construction types.

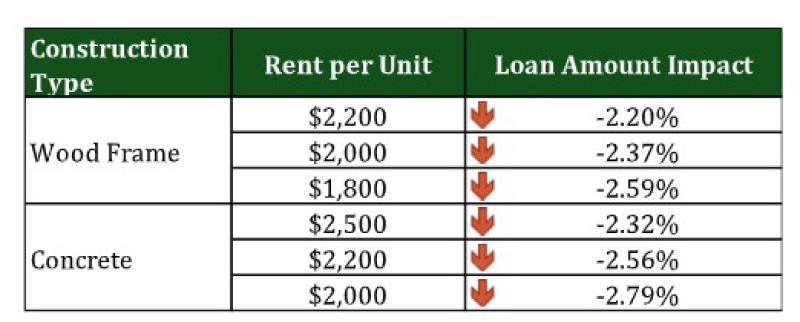

Quebec

Insight: Quebec shows the highest sensitivity, with the most pronounced reduction in loan proceeds among all regions analyzed.