More than 10 million square feet of Canadian office space has been converted, demolished, put into the pipeline for redevelopment or rumoured to become so, according to Avison Young's principal and director of market intelligence for Canada, Marie-France Benoit.

That figure explains only part of what's been a significant structural shift in the country's commercial real estate market since the pandemic.

But as office leasing gradually stabilizes and the most conversion-ready building stock shrinks, the question is whether the conditions that made them work are still in place.

Benefits beyond housing

If all planned and rumoured projects proceed, Benoit estimates approximately 17,000 new residential units would be added to Canadian housing stock. Not enough to resolve the housing crisis on its own, she acknowledges, but the value extends beyond raw unit counts.

"It's also urban revitalization," she noted, describing how vacant, obsolete class-C buildings become hotels, student housing and residential projects that bring pedestrian activity back to city cores — particularly Calgary's, where changes have drawn significant new downtown residents.

But the conversion story isn't uniform across the country.

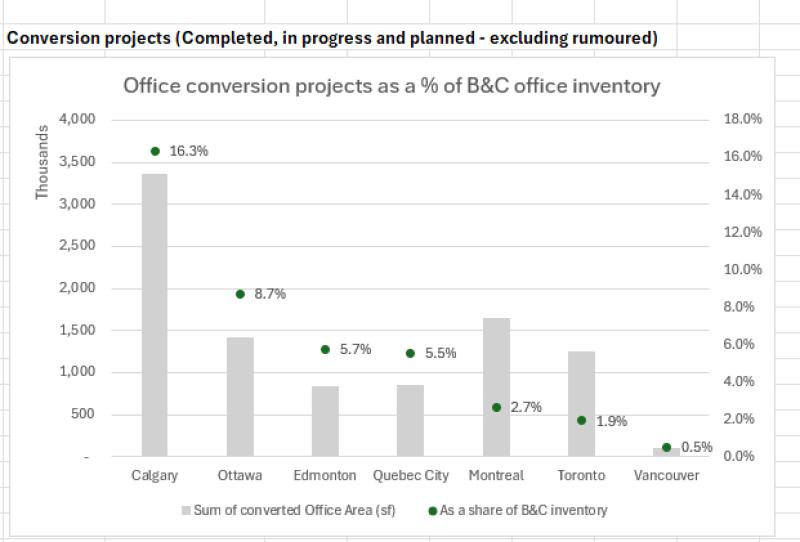

Conversions by region

In Toronto, Benoit says the predominant model involves demolishing older, obsolete office buildings to make way for high-density, mixed-use or residential towers — a function of expensive land that incentivizes maximum density.

In Ottawa and Calgary, it's more often the building shell that remains, with interiors gutted and rebuilt as multi-residential units.

Calgary occupies a category of its own. The city was already grappling with elevated downtown office vacancy before COVID-19 arrived — sitting at roughly 20 per cent when its conversion program launched, according to Benoit.

The municipal grant program, which offers $75 per square foot to developers undertaking conversions, has made the financial case where it might otherwise have failed.

Geoff Kallweit, a principal at RJC Engineers, described it as creating "a special environment" in a city with "lots of available building stock, some incentive to do it and a high demand for residential. The three things together make (Calgary) still quite attractive," he observed.

Nearly a dozen class-B office buildings have been successfully converted in Calgary's downtown core, according to Kallweit, who has worked on multiple such projects.

Ottawa has taken a different approach, streamlining the approval process and implementing as-of-right zoning for conversions rather than offering direct financial subsidies, Benoit said.

The result, she added, has been notable, with roughly one million square feet of older class-B and -C inventory in downtown Ottawa either complete, under construction or planned for conversion — representing nearly 10 per cent of that inventory class.

She described Vancouver as largely absent from the conversion conversation, for reasons both structural and economic. The only conversion Avison Young has tracked in Vancouver was an office-to-hotel transaction.

Benoit explained the city lacks the aging office inventory found in eastern markets, and land values are too high to support the economics of keeping existing structures. Plus, Kallweit adds, the high-seismic zone that Vancouver's in, introduces complexity and cost to any retrofit.

Conversion challenges

Regardless of location, when it comes to conversion potential, a building's physical characteristics matter enormously.

Kallweit points to floor-plate size as a primary filter: residential conversions require window access for every unit, which large, deep floor plates make difficult or expensive to achieve.

The average conversion candidate nationally, according to Benoit's data, was built around 1966 and has a floor plate of roughly 12,000 square feet — old enough to be economically obsolete for office use, compact enough to adapt for residential.

"You've got to redo all of that," Kallweit emphasized, adding that while the complexity is real, experienced developers treat it as a challenge to manage within the process rather than a reason to walk away. He's seen Calgary developers complete the process five times or more.

The future of office and the return of institutional capital

The broader office market has begun to shift in ways that affect conversion economics, according to Benoit.

Demand is recovering, she says, but it's highly concentrated in trophy and class-A space. Class-B buildings — the primary conversion candidates — remain at double-digit vacancy in most markets, while class-C space, that can't compete for modern tenants, continues to move toward its highest and best use case, like residential, hotel or student housing.

What's changed most visibly in the past few years, she says, is the return of institutional capital to straightforward acquisitions: buying quality buildings as office assets, not conversion plays. "There's more clarity now about the future of office. It's easier to envision what the market will look like five years from now than it was in 2022."

And that clarity is gradually redirecting capital. Conversions will continue, both Benoit and Kallweit agree, but driven by obsolescence, rather than pandemic-era panic.

As Benoit put it, the spotlight has moved: "The focus is on the big shiny towers," while the work of finding second lives for aging buildings carries on, building by building, city by city, wherever the economics allow.